Overview

Financial Regulation & Licensing

The full picture: FINMA licences, SRO membership and AML in one place, and how to tell which you need.

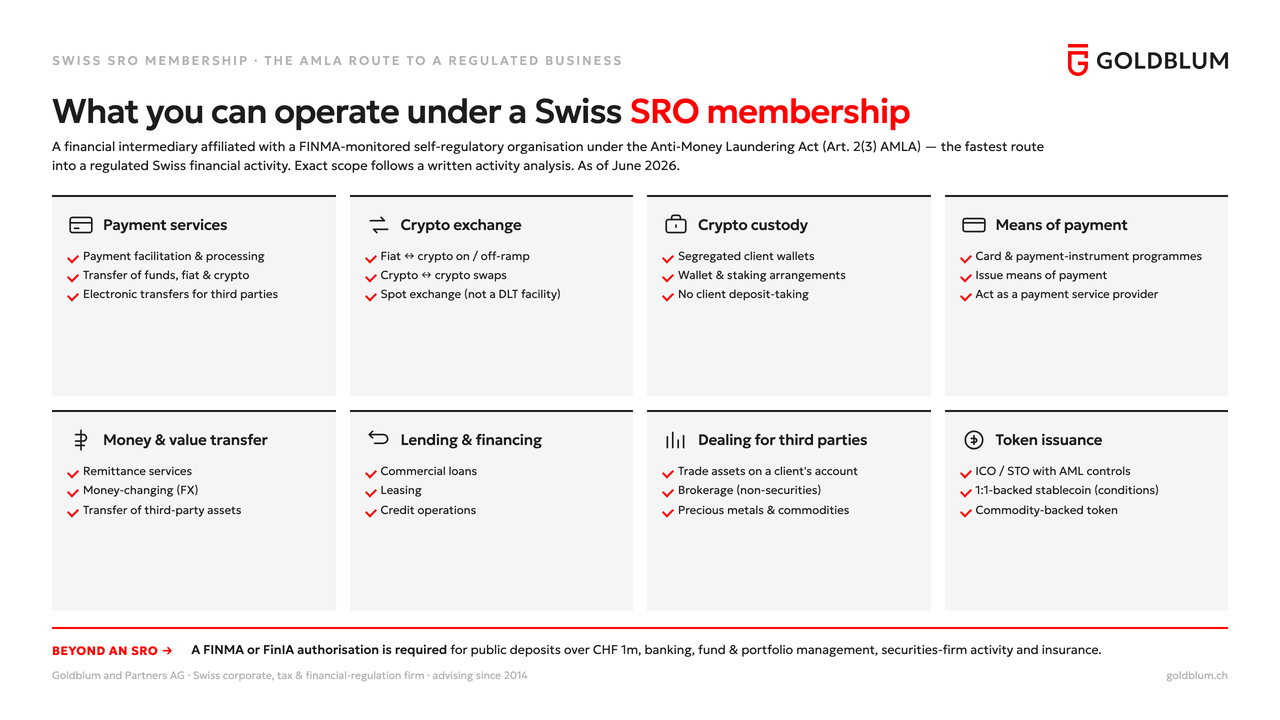

Financial Regulation overviewIf you handle other people’s money as a business but do not need a prudential FINMA licence, Swiss law still puts you under anti-money-laundering supervision. This catches crypto and token businesses, virtual-asset service providers (the EU calls them CASPs), payment and e-money providers, and money-service or escrow operators. The route is affiliation with one of the eleven FINMA-recognised Self-Regulatory Organisations. We confirm whether the duty applies, build the AML framework, choose the right SRO and carry you through admission.

An AML affiliation, not a prudential licence, granted by a private body that FINMA recognises and oversees.

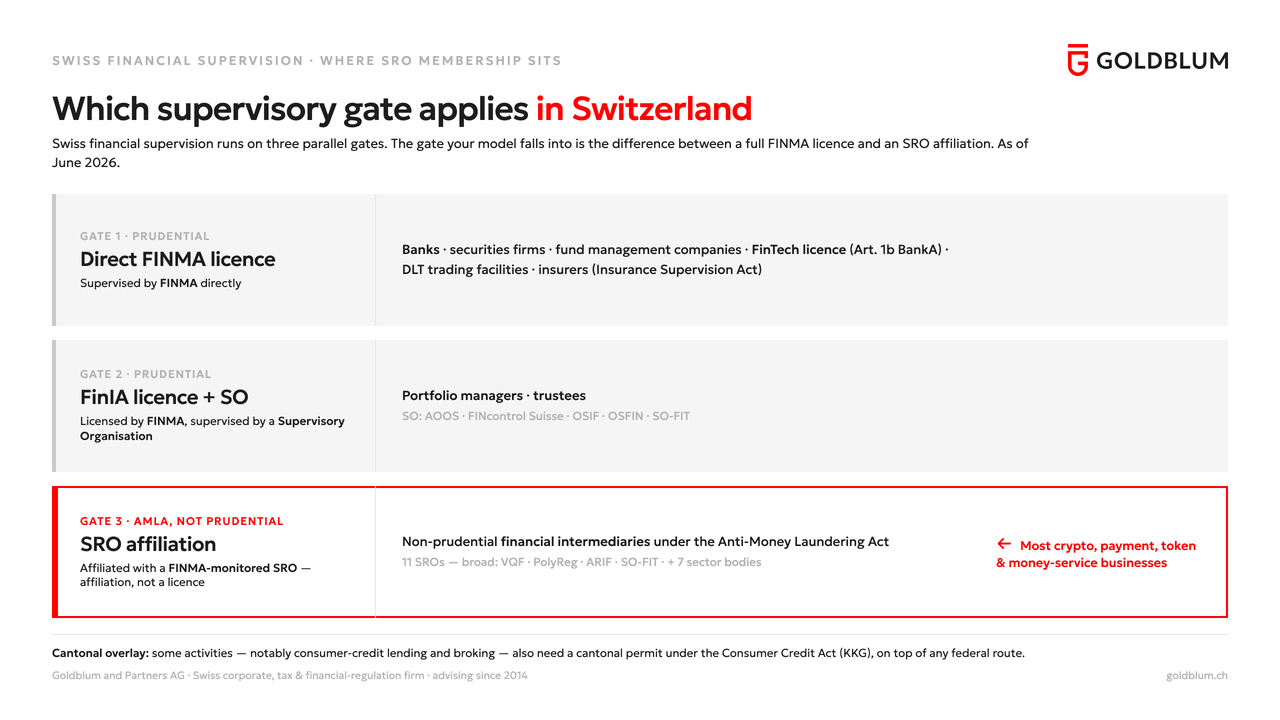

Before anything else, settle which regulatory gate your business goes through; the wrong door costs months. Switzerland supervises money-handling businesses through three of them. Two are prudential licences, granted and supervised by FINMA itself. The third is an SRO affiliation: an anti-money-laundering membership with a private body that FINMA recognises, not a licence. This page is about that third gate.

An AML membership FINMA recognises and oversees

For professional financial intermediaries that hold or move other people’s money but need no prudential licence: most crypto, payment, token and money-service businesses. You affiliate with one of the eleven FINMA-recognised Self-Regulatory Organisations (such as VQF), which issues binding AML rules and audits your compliance.

Authorised and supervised by FINMA itself

For deposit-taking and banking, fund management, securities-firm and DLT-trading activity, including the FinTech licence under art. 1b Banking Act. A prudential authorisation to carry on the activity: a heavier gate than an SRO.

Licensed by FINMA, supervised by an SO

For portfolio (asset) managers and trustees. Since 2020 they hold a FinIA licence and are supervised by a Supervisory Organisation (SO), not an SRO. The common confusion: managing clients’ money is Gate 2, not Gate 3.

Two things sit alongside the gates. Insurance has its own route: undertakings are authorised under the Insurance Supervision Act and intermediaries entered in FINMA’s register. And some activities, notably consumer-credit lending and broking, also need a cantonal permit under the Consumer Credit Act (KKG) on top of any federal gate. If you only advise, or never touch your customers’ money, you may be outside the net altogether; the check further down tells you which.

A Self-Regulatory Organisation (SRO) is a private body, recognised and supervised by FINMA, that admits and audits financial intermediaries for anti-money-laundering purposes under the Anti-Money Laundering Act. If your business accepts, holds or helps transfer assets belonging to others on a professional basis, and you do not hold a prudential FINMA licence, you must affiliate with an SRO before you operate. There are eleven recognised SROs as of July 2026 (FINMA's register was last updated 16 July 2026), and choosing between them is worth getting right.

The duty only bites once the activity is carried on professionally. The Anti-Money Laundering Ordinance sets de-minimis thresholds: gross profit above CHF 50,000 a year, business relationships with more than 20 contracting parties in a year, unlimited power of disposal over third-party assets above CHF 5 million at any time, or transactions exceeding CHF 2 million in a calendar year. Crossing any single threshold makes the activity professional and triggers affiliation.

Until the end of 2019, a financial intermediary could choose to be supervised for anti-money-laundering directly by FINMA (the “directly-subordinated” or DSFI status). The FinSA/FinIA reform abolished that route on 31 December 2019. Since 1 January 2020, SRO affiliation is the only way for a non-prudentially-licensed intermediary to meet its AML duties. For the businesses on this page, it is not one option among several but the route.

An SRO covers a wide band of money-handling models, subject to a written activity analysis. Similar-sounding services can sit on opposite sides of the line depending on custody, discretion and the character of the instrument, so the list below is the starting point, not the ruling.

Pick the plain description that fits your business. Two or three simple questions, then we tell you the likely route. No jargon, no legal advice. The binding answer always comes from a written review.

The short version. If your business handles other people’s money (sending or processing payments, letting people buy/sell/hold crypto, changing money, holding funds or assets, or lending), and you do not hold a full FINMA licence, you most likely need to join an SRO (an anti-money-laundering body recognised by FINMA). If you invest or manage money for clients, run a fund, or take deposits, you need a FINMA licence instead. If you only give advice or use your own money, you may need neither. Tell us what you do and we’ll confirm the route.

All eleven apply the same federal law, but they differ in sector focus, working language and location. Several are sector-specific; four (VQF, PolyReg, ARIF and SO-FIT) admit the broad range of parabanking intermediaries, which is where most crypto, payment and fiduciary businesses affiliate.

For a crypto, token, payment or money-service business, the realistic choice is one of these four. VQF is the largest and the default for most crypto and fintech affiliations; the other three are chosen mainly on working language and seat. The sector-specific seven (leasing, insurance, notaries, investment companies) will not admit a general crypto or payment model.

| SRO | Seat | Working language | Typical fit |

|---|---|---|---|

| VQF | Zug | German (English in practice) | The largest SRO and the usual home for crypto, token and fintech; broadest membership |

| PolyReg | Zurich | German | Tech-neutral; suits hybrid fiat-and-crypto and general intermediary models |

| ARIF | Geneva | French | French-speaking Switzerland; broad, fintech-friendly membership |

| SO-FIT | Geneva | French | Intermediaries and trustees in the Geneva region |

On fees, VQF is representative of the range: an admission processing fee of about CHF 1,800 and a minimum annual fee in the region of CHF 1,250, with file- or turnover-based components on top; the other three sit in comparable territory. The choice turns on working language, where supervision sits most comfortably for your model, and the activity mix — not on price alone. We match the SRO to the business and run the affiliation through to admission.

| SRO | Typical members | Contact |

|---|---|---|

| | Broadest membership, including crypto and fintech; the largest SRO. | General-Guisan-Strasse 6, 6300 Zug +41 41 763 28 20 info@vqf.ch vqf.ch |

| | General financial intermediaries; tech-neutral, suits hybrid fiat-and-crypto models. | Florastrasse 44, 8008 Zürich +41 43 488 52 80 info@polyreg.ch polyreg.ch |

| | French-speaking Switzerland; broad membership, fintech-friendly. | Rue de Rive 8, 1204 Genève +41 22 310 07 35 info@arif.ch arif.ch |

| | Financial intermediaries and trustees in the Geneva region. | Rue Pedro-Meylan 2, 1208 Genève +41 22 700 73 20 info@so-fit.ch so-fit.ch |

| | Supervision body also recognised as an SRO. | Clausiusstrasse 50, 8006 Zürich +41 44 215 98 98 info@aoos.ch aoos.ch |

| | Members of the Treuhand Suisse fiduciary association. | Monbijoustrasse 20, 3011 Bern +41 31 380 64 30 info@treuhandsuisse.ch treuhandsuisse.ch |

| | Ticino fiduciaries and intermediaries (Italian-speaking). | oadfct.ch |

| | Lawyers and notaries (Bar Association & Notaries). | sro-sav-snv.ch |

| | Life insurers (Swiss Insurance Association). | sro-svv.ch |

| | Leasing companies (Swiss Leasing Association). | leasingverband.ch |

| | Investment companies (Verband der Investmentgesellschaften). | svig.ch |

For most internationally-owned crypto, payment and asset-holding businesses the realistic choice narrows to VQF, PolyReg, ARIF or SO-FIT. We match the SRO to the activity, language and risk profile rather than defaulting every client to the same one, or you can approach a body directly using the details above.

Affiliation attaches to a real Swiss entity with genuine substance, not a letterbox. Five things have to be in place before an SRO will admit you:

A five-phase, deliverable-driven process. The work is front-loaded into the AML framework; once that file is sound, admission is comparatively quick: two to four months from a ready framework, as of June 2026. The variable is the quality of the file, not the SRO. Per-step timings are indicative and often overlap.

Business-model assessment and written qualification across the FINMA licence categories and the SRO/AMLA framework, including selection of an appropriate SRO.

Registered seat, board signatory and MLRO, auditor nomination, outsourcing controls, and interaction with the Supervisory Organisation where FinIA applies.

AML/KYC, sanctions screening, transaction monitoring and record-keeping; onboarding documentation and a training plan; consistency across SRO, FINMA registers and the website.

Preparation of the SRO admission (or FINMA licence) dossier; handling of regulator queries; alignment of client-facing materials with the applicable framework.

Operational integration and KPI reporting to the board; pre-audit reviews ahead of the initial and subsequent SRO/AMLA audit cycles; the first AML audit falls within the first year.

There are two layers. The first is the SRO’s own schedule: an admission fee plus a recurring annual fee, with file- or turnover-based components on top. VQF, the largest SRO, publishes an admission processing fee of about CHF 1,800 and a minimum annual fee in the region of CHF 1,250 (as of June 2026); file-based fees run in tiers of roughly CHF 30, 20 and 10 per file, and turnover-based fees range from about CHF 500 to CHF 10,000. An external AML audit, charged by time, sits on top each year. These are VQF’s published figures as of June 2026; each SRO sets its own tariff, so the exact numbers turn on which body you join.

The second layer is standing up the firm and the AML framework. For a crypto or payment business, first-year costs commonly run to CHF 50,000–150,000 once company set-up, the framework, admission, the first audit and advisory are counted. We quote a fixed advisory budget against a confirmed activity, so the number is settled before any work begins.

Ask for a fixed budgetAffiliation is not a one-off filing. As a member you carry continuing anti-money-laundering duties, which the SRO audits:

If the activity is really managing third-party portfolios, running a fund or taking deposits, you need a FINMA licence: back to Gate 1 or Gate 2 above, not an SRO. If your crypto or payment activity will fall under the 2027 Crypto-Institution or Payment Instrument Institution categories, an SRO affiliation may be only an interim step before a direct FINMA licence. We say which gate you are in before you spend on a framework you do not need.

Two things decide whether an SRO affiliation goes well: scoping the right route before any cost is committed, and carrying the AML function long after the certificate arrives. We have done both since 2014.

IFLR1000, a leading international directory of financial and corporate practices, has recognised the firm across editions since 2015 for its corporate, restructuring and financial-services work.

We analyse the model under AMLA, FinIA, FinSA and the Banking Act before launch, so the route (SRO or a FINMA licence) is settled from the outset, not discovered later.

We can act as your external AML Officer (MLRO), run the periodic audits and keep the framework current. Licensing is the start of the relationship, not the end.

Serving as your outsourced AML Officer under mandate: red-flag escalation, the SAR/MROS process, and reporting to the board.

Preparation and coordination with the auditor or SRO, development of remediation plans, and follow-up through to close-out.

Onboarding and conduct materials: KYC questionnaires, source-of-funds and wealth declarations, PEP and sanctions notices, risk warnings, fee disclosures, terms and engagement letters.

Drafting and managing responses to FINMA or the SRO, submission of notifications and updates, and assistance with bank or PSP due-diligence requests.

Induction and periodic AML training, attendance tracking, short assessments, and role-based modules for front office, operations and management.

Outsourcing register, a roles-and-responsibilities matrix, monitoring checklists, and a documented audit trail of file reviews and remedial actions.

Non-confidential mandates from more than a decade of Swiss financial-regulation work, dating back to 2014: SRO affiliations, FINMA and FinIA licensing, and regulatory enquiries across crypto, payments, asset management and token projects.

SRO authorisation · FINMA non-subordination ruling

SRO authorisation · FINMA non-subordination ruling FinIA licence

FinIA licence SRO authorisation · FINMA non-subordination ruling

SRO authorisation · FINMA non-subordination ruling SRO authorisation · FINMA non-subordination ruling

SRO authorisation · FINMA non-subordination ruling SRO authorisation · FINMA non-subordination ruling

SRO authorisation · FINMA non-subordination ruling SRO affiliation

SRO affiliation SRO affiliation

SRO affiliation SRO affiliation

SRO affiliation SRO affiliation

SRO affiliation

Listed with each client’s agreement (non-NDA). Engagement details are kept general; specifics are covered by professional confidentiality.

The full picture: FINMA licences, SRO membership and AML in one place, and how to tell which you need.

Financial Regulation overviewTell us the activity and we say which gate applies (SRO, a FINMA licence, or neither) before you spend on a framework.

Request an assessmentRated 5.0 / 5 from 38 reviews on Google. Read them on Google →

“Perfekter Service! Wir wollten eine AG in der Schweiz übernehmen und hatten kaum Zeit – innerhalb weniger Tage war alles organisiert, inklusive Notar, Handelsregister und Bank.”

“We consulted Goldblum and Partners for structuring our crypto project under Swiss law. Their team was clear about the threshold between non-custodial and financial-intermediary status.”

“Équipe sérieuse. La documentation AML fournie était claire et adaptée à notre activité crypto. Je recommande.”

“Professionisti veri. Conoscono bene la legge svizzera e si sono occupati di ogni aspetto del passaggio azionario.”

Send us a two-line description of what the business does. A partner confirms whether it is financial intermediation on a professional basis, and which of the 11 SROs fits, before you commit to anything.